Lexington Board of Selectman on tax and employee benefit

By Joe Pato

Posted Apr. 26, 2016 at 12:23 PM

LEXINGTON

Joe Pato is the chairman of the Board of Selectmen and submitted this on behalf of the board

Opponents of the May 3 debt exclusion vote argue that the town can and should change how it taxes commercial properties, chooses to implement the residential tax exemption and packages employee health benefits before it requests a debt exclusion from voters for the three elementary and two middle school projects. These tax and employee benefits proposals have been floated for many years and are impractical. The Board of Selectmen believe these proposals are bad municipal policy and irrelevant to the May 3 debt exclusion vote.

Our proposals to save $3.8 million in taxpayers’ money and to lower taxes on small homes are not “impractical”. Had they been implemented, no extra tax increase would be needed on May 3rd to fund $71 million in school construction.

Commercial assessment

Lexington follows assessment regulations imposed by the Massachusetts Department of Revenue. Straying from strict adherence to these rules would likely lead the Appellate Tax Board to grant an abatement if a property owner contests the assessment. These abatements include an 8 percent yearly interest payment on all overpayments and represent a significant financial risk for the town.

Opponents contend that Lexington officials should advocate for changes in the DOR regulations to more directly rely on commercial property sales. This is impractical – many communities like Lexington have too few commercial properties sold each year to establish clear values for comparable properties.

The Board seeks to achieve a balance between residential and commercial tax-payers by encouraging sustainable growth in our commercial and industrial zones. We have recently seen construction begin on the first new building in 40 years on Hartwell Avenue and another building is undergoing major renovations. In addition, Lexington takes full advantage of the split tax rate option and imposes a commercial tax rate that is roughly twice the residential tax rate.

We don’t ask Lexington to “Stray[...] from strict adherence to [the Massachusetts Department of Revenue] rules”. Rather, the Selectmen must work with the Legislature to update DOR’s outmoded rules on assessments of large commercial properties, which create unwarranted tax breaks. How does Joe Pato know that this “is impractical” since the Board has not studied it in detail, nor petitioned the Legislature?

Commercial properties are taxed at twice the residential tax rate, as State rules allow (CIP factor, or split tax rate), but taxes actually paid are half of what they should be because commercial assessments are well below market values: the Giroux building is assessed at 41% of its sale price while most houses are assessed at 90% of theirs. Joe Pato conflates split tax rate and fair assessments, which are unrelated issues.

Residential exemption

The residential exemption allows the Board of Selectmen to exempt up to 20 percent of an owner-occupied residential property’s value from taxation. The exemption applies only to owner-occupied properties. The effect of electing this exemption shifts residential property tax burden onto larger homes, vacant land and rental property. This exemption is used in a small number of communities — mostly cities — where a large inventory of rental or vacation property is located.

There are no income or means tests associated with this exemption. In Lexington, where some residents live in a home that they have transferred to a trust or where the value of the home has appreciated significantly over the years, the residential exemption could have the counter-intuitive effect of raising taxes on residents of limited means.

The board considers this exemption every year and will continue to do so. They are also investigating and encouraging the legislature to adopt other programs that provide means-tested property tax relief. In the meantime, the board encourages residents to explore existing tax-relief programs that can be found on the town’s website, lexingtonma.gov/assessor.

The “small number of communities” (whether cities or towns makes no difference) with a residential exemption account for 18% of Massachusetts’ total population. Like Joe Pato, we would prefer a means-tested mechanism to cut taxes on people who need it, but the residential exemption is the only mechanism now available to cut taxes on large numbers of taxpayers; waiting for the perfect (means-tested) solution is a poor excuse to not do what’s possible and fair now, a residential exemption.

Not having a residential exemption in Lexington is in itself a choice. In Lexington, we have many more people on limited incomes in small houses (who need tax relief) than “house rich, cash poor” people. If a residential exemption makes it difficult for “house rich, cash poor” people to pay (higher) taxes, they can reverse mortgage their home, borrow from their heirs or move to a smaller house.

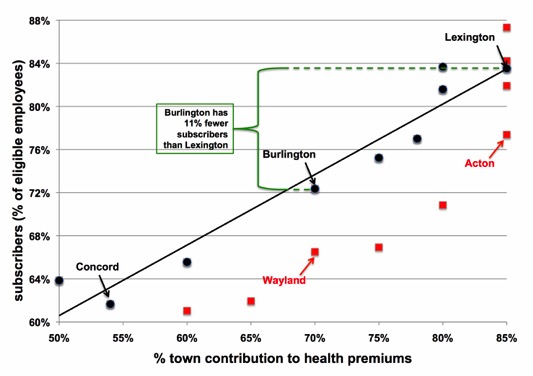

Opponents suggest that reducing the employer percentage contribution for employee health insurance premiums would result in fewer employees electing to take advantage of the benefit. This is based on data from a small number of communities (18) and eliminating half of those from the statistical analysis. This is a questionable methodology.

In early 2010 we interviewed 18 communities and found these results (details here):

If 18 is too few communities, Town staff should survey more. Each red dot represents a community that had a cash plan (similar to what Joe Pato describes below), which, we were told, is helpful but skews the data because employees view a cash plan as temporary, unlike the union-negotiated share of health premiums the town will pay (85% in Lexington) which is considered permanent.

We would love to hear from the Board of Selectmen what a less “questionable methodology” would be. Absent one, our detailed model is very robust, even if certain parameters have changed (premiums are lower now because Lexington has joined GIC; we have more employees in Lexington as time passes; etc).

Rather than be defensive on this multi-million-dollar savings opportunity, the Board and Town staff should urgently conduct all necessary analyses to fully understand this problem and solve it via union negotiation with our employees in a manner beneficial to all parties.

Lexington has instituted a program in 2015 by which employees can opt out of health care benefits in return for receiving a small cash payment. This program is working well. Lexington provides a total compensation package including salary and benefits negotiated with our employee unions that is competitive with our neighboring and peer communities.

We applaud that “Lexington has instituted a program in 2015 by which employees can opt out of health care benefits in return for receiving a small cash payment” — albeit several years later than many communities — but communities have found such plans to be far less effective than permanently lowering town contribution to health premiums and raising salaries to keep total employee compensation unchanged.

Conclusion

The Board of Selectmen unanimously recommends voting yes on the debt exclusion question on May 3. We don’t believe that the tax and employee benefit policy recommendations being offered by opponents of the debt exclusion are good municipal policy nor are they relevant to the debt exclusion question.

The Board’s “belief” is incorrect for the reasons this web site outlines. Our policy recommendations are directly relevant to the extra tax increase requested on May 3rd because if they had been implemented, no extra tax increase would be needed.

Note on school capacity optimization

Joe Pato did not address this problem, perhaps because it is the direct responsibility of the School Committee, not the Board of Selectmen.

But the Selectmen are responsible for the town’s budget and for requesting tax increases (via operating overrides and debt exclusions), so they should carefully monitor how many elementary classrooms will exist on Oct 1, 2016 (for 2016-17) — as we will — to ensure that half of our classrooms no longer have fewer than “preferred” number of students, unnecessarily costing Lexington’s budget $1.5 million annually.